Following our biggest conference yet, which was dedicated to real estate financing through various regulatory and tax structures and where we also addressed the establishment and operation of funds, we gave a lecture with Vladimíra Mačuhová at the methodological days of the Chamber of Tax Advisors. However, in this lecture we focused on various tax aspects and situations related to the existence of not only domestic but also foreign funds.

For those who did not attend the conference, we have provided a more detailed overview of the topics covered at the conference in a separate article. The article can be found at this link. At the same time, if you would like to watch the whole conference, or just some parts of it, we have video recordings of the conference available for you, which can be found at this link.

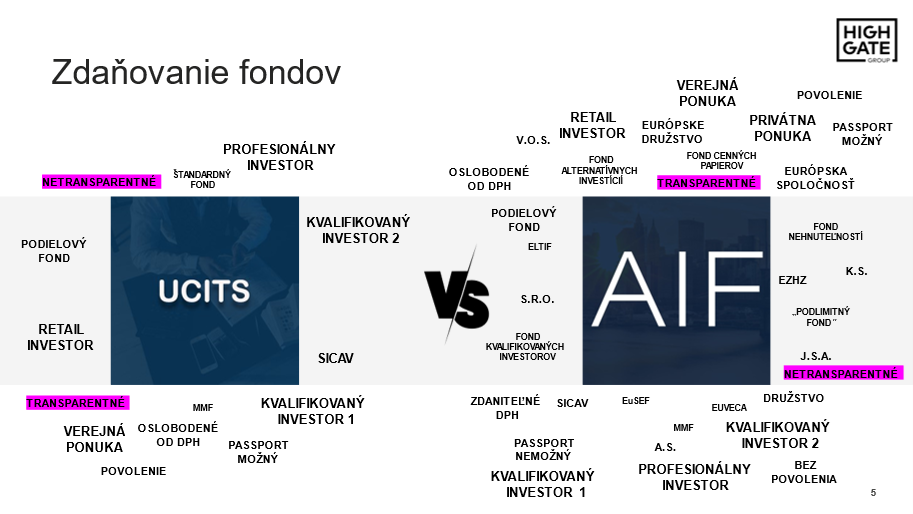

The form and amount of taxation for Slovak funds depends primarily on the legal form of the fund. By default, there are transparent and non-transparent forms, whereas in the case of mutual funds we see a hybrid between the two.

It is the analysis of a fund’s tax set-up that can be crucial to the efficiency of the fund structure and ultimately the investor’s return.

During the lecture at the conference, as well as during the methodological days of the Chamber of Tax Advisors, we also devoted a certain part to various foreign fund structures and individual income from the perspective of classification according to Slovak tax and general legal regulations. In some fund structures, given the incompleteness of Slovak law, it may also be the case that the income from the fund, as well as the income of the fund itself, will not be taxed at any level.

In general, however, there are a number of non-tax reasons why fund managers or founders choose a foreign structure. At the conference we talked about the following:

Thus, taxes are only one consideration and should not be the primary consideration for purposes of defending a foreign fund’s tax position.

In the lecture we discussed in detail the topic of management fees in fund management. The problem with the interpretation of our VAT Act was caused by the Slovak legislator who forgot to amend the VAT Act when introducing the SICAV legal form. Today, in principle, funds in Slovakia may face the risk of a mechanical interpretation that would be contrary to EU law and could significantly harm the fund structure (including investors).

However, it is important to note that not every fund administration is exempt from VAT, and in practice it is relatively common to find that trustees (including institutional trustees) are not sufficiently knowledgeable on the subject. When setting up the fund structure, it is therefore essential to bear this in mind and try to set up the structure as efficiently as possible within the legal framework.

If you are interested in this topic, please do not hesitate to contact us.