We strive to set up our clients’ businesses in a tax and levy efficient manner. However, we are not only concerned with optimization from a tax perspective, but also in terms of legal challenges and practical implications. As we have been dealing with this topic for a long time and on various fronts, it is also one of the focus topics in our external lectures or at our business conferences, including the largest in Slovakia legal and tax conferencewhich we had the honour to organise and lecture at. We comment on this topic in Media, we write articles and lectures or organize training and webinars.

In general, tax optimisation must be based on real business or legal reasons. It simply has to be “honest” in order to be defensible before the tax authorities or the courts. In such a case, it qualifies for the set of so-called The state cannot now and will not be able to perceive them as non-compliant with the law in the future. If you are deciding between an LLC or a sole proprietorship, this is a legal and legitimate tax optimization. The same applies in the case of selling, for example, a shopping centre, where you can choose between selling the company or transferring the so-called “company”. You can choose between buying the business or selling the business. These are legal and legitimate ways of managing your overall tax and levy liability. However, if you decide to run, for example, 10 non-VAT businesses to avoid VAT registration, this is already aggressive tax optimisation. And one that can, in certain circumstances, have criminal implications. For example, if you decide to set up a company in a country with a lower tax burden without operating any business there, that can have negative tax and, in certain circumstances, criminal implications as well.

For example, we assist clients in the area of tax and levy optimization in the following specific topics:

If you do business across borders, the possibilities for optimisation expand. Never in history has the physical movement of people and goods been as easy as it is today. In the same way, it has never been easier to provide services from one end of the world to a customer located on the other side of the world. In the world, borders are blurring, distances are becoming relative and many business opportunities are becoming more and more real. The open world thus brings opportunities to exploit countries’ tax advantages to optimise taxes, the flow of finance and asset protection.

However, international tax rules and regulation are constantly changing, with increasing globalisation complicating the taxation of both cross-border and domestic operations. Detailed knowledge of this regulation enables us to design and implement efficient and effective tax structures for our clients in cooperation with our foreign partners that meet current regulatory requirements.

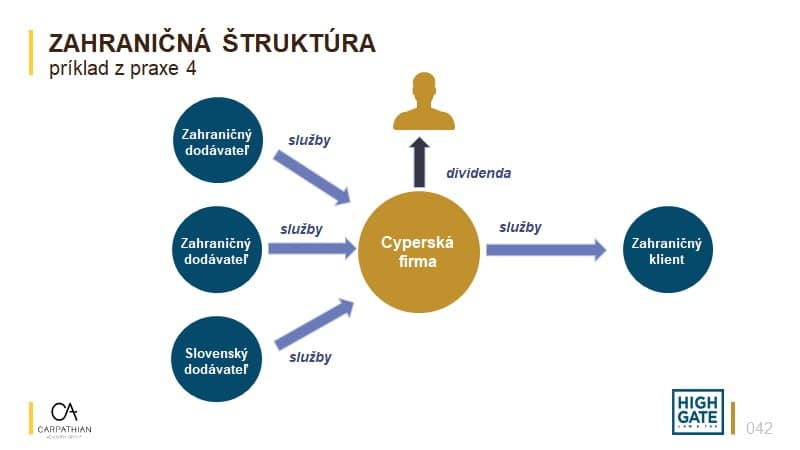

In particular, we provide our clients with the following cross-border tax optimisation services:

We mainly provide the following services to our clients:

An offshore company is not to be understood as a company incorporated and existing in the jurisdiction of one of the Caribbean islands. For example, a critical part of Czech holding companies, which until recently were often set up by Slovak tax advisors in order to avoid capital gains taxation in Slovakia in the event of a successful EXIT, can be considered offshore companies. Even the recent sale of a well-known Slovak IT company was made through an offshore company. This was the Austrian holding company in this case. An offshore company thus does not only include companies from the so-called. tax havens that have been set up for the purpose of reducing the tax liability of the entrepreneur.

An offshore company is any company that is not located in the country of the founder or in the country in which the functions and risks associated with the income generated by the offshore company are actually carried out. An offshore company can thus also be located in the Czech Republic as well as in the British Virgin Islands. Offshore companies are also set up to achieve a degree of anonymity. In the recent past, it was common to hide assets through offshore companies with the legitimate aim of protecting them from various vested interests or violent structures. In South America, but also in Russia or Ukraine, it is still relatively common today for many businessmen to conceal their property in order to protect their lives and the lives of their family members. The disadvantages of property transparency are also experienced by many entrepreneurs in Slovakia thanks to public access to company accounts.

There are relatively many cases where part of the assignment from our client was also to achieve greater anonymity of his property disposition. The reasons may be different. From those illegitimate motives mainly related to criminal activities, it is also the need to protect the entrepreneur and his family from the attention or unreasonable demands of his business partners or employees. Offshore companies are also set up with the intention of avoiding administrative or regulatory restrictions.

In Slovakia, for example, it happens relatively often that the commercial register does not function as the law commands. Filings are also delayed for unreasonably long periods of time, creating a legitimate demand for company formation in other countries. However, does this legitimise the use of a favourable tax regime abroad? Similarly for regulation. If Slovak or European legislation allows entrepreneurs to do business in certain areas (e.g.: securities trader or collective investment fund) only with regulatory difficulties, entrepreneurs look for more flexible offshore solutions.

Slovakia is a small country, which naturally does not have the professional infrastructure and ambition to create a full-fledged legislative framework for cryptocurrencies and related business.

The result is a legally uncertain environment that is uncomfortable, especially for larger projects. This is mainly due to the lack of predictability of the decision-making activities of the relevant Slovak authorities. That is why several Slovak projects in the field of cryptocurrencies and blockchain are considering moving their legal presence abroad. In that case, they create offshore companies.

Is it legal?

Can the state interfere with this freedom and force entrepreneurs to tax profits from abroad in Slovakia?

The establishment of an offshore company in any tax haven is not in itself illegal. However, its subsequent use may become illegal. In practice, fictitious back-to-back supplies of services from tax havens via the Netherlands or the UK to a Slovak company are still relatively common. The entrepreneur is thus able to shift profits from the 21% tax rate bracket (Slovakia) to the 0% tax rate bracket (tax haven).

On the other hand, there are situations where the use of a company based in a 0% tax country may be perfectly legal and legitimate. The fact that a country does not tax corporate profits cannot in itself be problematic.

As can be seen, for example, in the subservices Patent Box and optimization for IT and development companies or Supercomputing for research and development, a 0% effective rate is relatively easy for a taxpayer to achieve even in Slovakia.

However, in a given case, it is necessary to use such an offshore company for legitimate reasons (e.g.: PR, investor’s request, better legal environment, etc.).

Slovakia has gradually adopted a number of statutory amendments to discourage Slovak entrepreneurs from illegitimate use of foreign offshore companies, primarily for tax avoidance purposes. For example :

CFC rules for individuals

The purpose of the rules is to ensure that the individual behind a foreign offshore company taxes the profits of that foreign offshore company. You can see more about this topic, for example, in the video “Is it even worth having an offshore company today? Ak áno, komu a kedy?“. Peter Varga’s criticism of these rules can be found in the article My comments to the MoF (CFC rules for individuals).

CFC rules for legal entities

Probably many taxpayers are completely unaware of the existence of this institute. The purpose of these rules is to ensure that the profits of foreign offshore companies are taxed by a related Slovak company, provided that the involvement of such a foreign offshore company resulted from one or more actions that are not genuine or were carried out for the purpose of obtaining a tax advantage.

35% tax

Certain payments made by a Slovak company abroad are subject to 35% withholding tax in Slovakia. On the other hand, certain dividends, liquidation proceeds or distributions are subject to 35% tax for the Slovak recipient in Slovakia. This is why it is nowadays problematic to “just” use, for example, a company established in the United Arab Emirates.

The place of the actual wiring

Based on the analysis of the place of the actual management of the company, the tax administrator is able to attribute Slovak tax residency to the foreign company despite the fact that the company is legally established and existing under a different legal order.

Final beneficiary

When applying withholding taxes, the tax administrator may check whether the Slovak taxpayer has investigated who is the final recipient of the income paid. The aim is to prevent the use of shell holding companies or other intermediaries.

Transfer pricing

In Slovakia, the perception of transfer pricing is undersized. The OECD Transfer Pricing Directive provides for its use even in situations where the taxpayer would not normally expect it. These include, for example, various internal reorganisations and the transfer of activities from one company to another. Indeed, such activities should be taxed.

Many more

In addition to other technical provisions, laws as well as case law, it is also familiar with substantive instruments. These are different concepts of substantive fairness or abuse of discretion under which a tax administrator may, in certain circumstances, take action against a structure that in no way formally contradicts the language of the tax code.

The analysis of the possibility of using an offshore company in a particular environment for a particular client should not only include tax and accounting elements. It is also necessary to look at the structure from a legal and practical point of view.

Suppose a business wants to take advantage of the tax exemption on the gain from the sale of shares or business interests in Cyprus. If an entrepreneur does not want to invest in a relevant advisor, he can make do with the Internet and his Slovak accountant. He finds out on the internet that Cyprus does not tax these profits by default, he finds a company that will set up a Cypriot company and provide him with a registered office, and a Slovak accountant approves it.

However, if he involves a relevant tax adviser in this structure, he will find that this type of tax optimisation has a broader dimension. For example, the following questions arise:

Counsel brings to the whole context the necessary legal dimension in situations where the written law does not give a clear answer. When interpreting, it uses case law, analysis of various interpretations of law (teleological, grammatical, historical, etc.) as well as philosophy and theory of law, which are necessary to reach in unclear situations. For example, the following topics may be covered:

In addition, you also need to have relevant practical experience with tax optimisation. For example, the following aspects may also be involved:

Under Slovak tax law, not every illegal tax optimisation fulfils the elements of one of the tax offences. Similarly to the identification of what is and what is not lawful in reducing tax or levy liability, the boundaries between criminal and administrative law supervision (Tax optimisation – domestic and foreign options) in the commission of tax offences are not clearly delineated.

Unfortunately, Slovak tax law does not know of many cases where courts or prosecutors have looked in detail at identifying more precise boundaries. From a business point of view, it is not at all comfortable not to be able to foresee the penalty for a tax offence committed. In this context, imprisonment (in conjunction with the penalty of forfeiture of property) is certainly the most serious interference with human integrity.

The case of KTAG Andreja Kiskis a case in which a critical part of Slovak entrepreneurs can see themselves. From the perspective of the requirements of the rule of law, it is not so much the fact that the case may have been a criminal offence of tax and insurance fraud that is problematic, but that the previous practice of tax administrators and law enforcement authorities has not in any way suggested that the criminal threshold has been pushed to this level. The latter affects a huge number of entrepreneurs who are thus ultimately exposed to the potential arbitrariness of the State.

We provide our clients with comprehensive tax advisory and tax optimization services (Tax optimization – domestic and foreign options).

This includes, in addition to technical advice, legal analysis with an emphasis on the analysis of potential criminal risks.

These services are used by clients as standard in the following business process situations:

Example 1: A firm makes a profit. However, it does not pay the profit to the shareholder as a dividend, but gives it to the shareholder as a gift and thus avoids dividend tax. The legislation does not formally prohibit such action. We can consider it as:

Example 2: A well-known athlete moves to Monaco and becomes a Monegasque tax resident. However, he spends a large part of the year in Slovakia for various marketing events, sleeping in his Bratislava apartment or in hotels. If he does not pay taxes on his worldwide income in Slovakia, it is

Example 3: An entrepreneur has bought a family car on which he has deducted 100% of the VAT and treats 100% of the depreciation of the car as a tax expense. However, he uses the car exclusively for family transfers. This is

Example 4: An entrepreneur owns two companies. Before the end of the calendar year, preliminary results showed that one company was expected to make a profit of 1 000 and the other a loss of 500. Therefore, the entrepreneur decided to invoice 400 from the loss-making company to the profitable company for marketing services. He thus reduced his tax liability. This is

Example 5: An entrepreneur has set up a company on a Caribbean island with a 0% tax rate and from which he invoices his IT services to Slovak clients. However, the entrepreneur is mainly located in Slovakia when performing the services. These are:

Thanks to the Patent Box, IT companies that develop software and other R&D companies that develop various inventions and technical solutions can pay income taxes in Slovakia even at a rate of 10.5%. For example, if Slovak IT companies want to pay lower taxes, they do not have to come up with complex and administratively demanding cross-border solutions.

Peter Varga in his article “Slovakia can be a tax haven too!” he commented positively on Slovakia’s efforts to compete with other favourable tax regimes in Europe thanks to the Patent Box. But it is the Patent Box that has brought an important tool for legal and legitimate tax optimization, especially for Slovak IT companies. Although relatively late, Slovakia has been inspired by other IP Box regimes with which other countries in Europe have been attracting added value to their territory for a relatively long time.

The Patent Box exempts from income tax up to 50% of the profits that the taxpayer makes from royalties for the grant of a right to use or for use:

The Patent Box also allows taxpayers to benefit from this exemption from income tax if they derive income from the sale of products which are the result of research and development carried out by the taxpayer and which are wholly or partly based on an invention protected by a patent or a technical solution protected by a utility model.

The patent box is a new instrument to support research and development in Slovakia, which makes it possible to exempt revenues from the provision of intangible assets (the so-called licensing revenues) and revenues from the sale of products for the production of which a patent or utility model is used from corporate income tax, up to 50% of these revenues. In other words, if a Slovak company accounts correctly and meets other conditions, it can qualify for the benefit of taxing profits at 10.5% instead of the standard 21%.

The Patent Box thus exempts from income tax up to 50% of the profits that the taxpayer earns from royalties for the grant of a right to use or for use:

The Patent Box also allows taxpayers to benefit from this exemption from income tax if they derive income from the sale of products which are the result of research and development carried out by the taxpayer and which are wholly or partly based on an invention protected by a patent or a technical solution protected by a utility model.

The taxpayer can achieve an effective tax rate of 10.5% through the Patent Box. As we often combine the Patent Box with theR&D Super Deduction for our clients, the effective tax rate can be 0% for several years.

Let us imagine a situation where an IT firm carries out an experimental development after completion of which it has licensing revenue. Assume that the company will record revenues and expenses as shown in the table below (amounts are in EUR):

| ROK | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

|---|---|---|---|---|---|---|---|

| Proceeds from the sale of licences | 0 | 0 | 200 000 | 500 000 | 750 000 | 1 000 000 | 1 200 000 |

| Relevant R&D costs | 250 000 | 250 000 | 0 | 0 | 0 | 0 | 0 |

| Write-offs | 0 | 0 | 100 000 | 100 000 | 100 000 | 100 000 | 100 000 |

| Other costs | 25 000 | 50 000 | 75 000 | 100 000 | 125 000 | 150 000 | 175 000 |

| Profit | 25 000 (loss) | 50 000 (loss) | 25 000 | 300 000 | 525 000 | 850 000 | 925 000 |

| Supercomputing | 625 000 | 625 000 | 12 500 | 150 000 | 262 500 | 425 000 | 400 000 |

| Tax | 0 | 0 | 0 | 0 | 0 | 0 | 13 125 |

| Effective rate | 0 % | 0 % |

The basic prerequisite is to carry out R&D activities and to account for them correctly. Based on our experience, mainly from audits of the accounts of young IT companies, we have observed a number of cases where such companies have incorrectly accounted for software development. Not only does this commit an offence under the Accountancy Act for which they are liable to a fine of up to 2% of the value of their assets, incorrect accounting can also unjustifiably reduce a business’s tax liability and disqualify them from using the Patent Box.

It is therefore essential to account for the Patent Box correctly and to anticipate its use in advance. Moreover, the relevant Patent Box provisions indicate in several places a requirement for the taxpayer to exploit its own research and/or development result. In other words, the Patent Box requires that only employees of the taxpayer are part of the personnel apparatus that produces the relevant intangible R&D results.

Due to the high tax-tax burden on labour, it is naturally more economically advantageous for taxpayers to reach for so called. contractors (i.e. self-employed, sole proprietorships)where the tax and levy burden is significantly lower. In certain circumstances and with well-drafted contracts covering the creation of works and other intangible results, the requirement for employees may be waived. Therefore, if a taxpayer does not work with an attorney who is knowledgeable about Patent Box issues, it may have a negative impact on the use of Patent Box.

The Patent Box should therefore be seen as an instrument whose statutory application affects not only tax law but also accounting and intellectual property law.

This is a very complex topic from both a legal and tax and accounting point of view. It was discussed in detail by Peter Varga at the recent methodological days of the Slovak Chamber of Tax Advisors, where he also lectured on the topic of the Patent Box together with a representative from the Ministry of Finance of the Slovak Republic and where the topic of the use of the so-called “patent box” was also outlined. freelancers(sole traders or trading companies). In certain circumstances, a company may use such outsourcers without reducing its Patent Box tax benefit. However, it needs to adjust its factual and legal position accordingly.

We deal with the topic of Patent Box relatively frequently. We write articles on the topic and give commercial or methodology talks. You can find more information in our articles and media releases or videos and conferences.

Working with our lawyers, we provide the following Patent Box services to our clients:

The origins of the Patent Box can be traced back to the 1970s in Ireland. years of the last century. Legislation at the time allowed companies licensing certain forms of intellectual property to reduce their income tax. The concept has been gradually applied by other countries, including France, Luxembourg, Cyprus and the UK. Recently, it was quite common to set up an offshore company in Cyprus, for example, and benefit from a reduced tax rate of 2.5% on income from the use of intellectual property when invoicing within the group.

The Patent Box concept is very popular today legislatively. Everywhere, however, the so-called. nexus principle, which prevents tax abusive practices. As can be seen from the figure below, Slovakia ranks among the progressive countries in this respect.

We have worked on a number of “blochchain based” projects. For example, the following projects:

For more information about our cryptocurrency practice, please visit Highgate Group. Anyway, even R&D activities of programmers in the field of blochchain can in principle qualify for the Patent Box regime.

The crypt area cannot be seen in isolation. Although it often falls outside the standard recognisable world, it is necessary to attribute to it the corresponding legal and tax frameworks.

One such framework is the Patent Box or Supercomputing (R&D Superdeductible).

Assume that the taxpayer spends the following amounts on R&D activities:

The Income Tax Act allows the taxpayer to reduce the tax base by:

The total amount of the super deduction which reduces the taxpayer’s tax base is EUR 245 000.

The taxpayer can thus save EUR 51 450 in income tax for the year.

The taxpayer can achieve an effective tax rate of 0% through the Super Calculation. As we often combine the Super Calculator with the so-called. Patent Box, the effective taxation can thus be below 5%.

Imagine a situation where an IT firm carries out experimental development after completion of which it has licensing revenue. Assume that the company will record revenues and expenses as shown in the table below (amounts are in EUR):

| ROK | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

|---|---|---|---|---|---|---|---|

| Proceeds from the sale of licences | 0 | 0 | 200 000 | 500 000 | 750 000 | 1 000 000 | 1 200 000 |

| Relevant R&D costs | 250 000 | 250 000 | 0 | 0 | 0 | 0 | 0 |

| Write-offs | 0 | 0 | 100 000 | 100 000 | 100 000 | 100 000 | 100 000 |

| Other costs | 25 000 | 50 000 | 75 000 | 100 000 | 125 000 | 150 000 | 175 000 |

| Profit | 25 000 (loss) | 50 000 (loss) | 25 000 | 300 000 | 525 000 | 850 000 | 925 000 |

| Supercomputing | 625 000 | 625 000 | 12 500 | 150 000 | 262 500 | 425 000 | 400 000 |

| Tax | 0 | 0 | 0 | 0 | 0 | 0 | 13 125 |

| Effective rate | 0 % | 0 % |

To qualify for the super deduction, the taxpayer must carry out one of the following research and development activities:

In order for a taxpayer’s research and development activity to meet the necessary characteristics, it is important that it has the following elements:

As legal and economic advisors, we are naturally unable to assess whether a client’s activity meets the characteristics of a research and development activity. Nor should it fall within the client’s remit because of conflicts of interest.

We therefore cooperate with the Czech company RESEA, which specializes only in research and development activities. Its task is to assess whether the case is indeed a research and development activity and to prepare all the necessary technical documentation.

The tax authorities currently have minimal experience with superannuation. They are therefore looking for inspiration in cooperation with the Czech tax administration, which, after so many years, has a relatively rich experience in tax audits and litigation with taxpayers before the courts.

Therefore, in preparing the taxpayer for a potential tax audit, it is important to anticipate and set up the documentation and processes already in the process of implementing the super tax calculation, taking into account the existing practice in the Czech Republic. That is why we cooperate with the Czech company RESEA, which has been working on this issue for almost 15 years.

It is important to note that the procedural position of the taxpayer under the Tax Code is against the taxpayer at the first stage. If the tax administrator raises doubts about the legality of the application of the super deduction, the taxpayer has the burden of proof to prove its claims in the tax return. If the burden of proof is not sustained, it is up to the tax authority to prove otherwise.

In cooperation with our lawyers, we represent clients in a range of tax proceedings, from representation at tax audits to court proceedings where the client must be represented by an attorney.

Thus, in cooperation with us on the supercomputation, the client receives an absolutely comprehensive service from the analysis, through the setup, the tax calculation, to the eventual representation to the European Court of Human Rights.

Complexity:

Technical documentation:

A broad team: