Even if a company does not cheat on VAT and complies with tax regulations, the tax authorities may not recognise its right to deduct VAT or may charge VAT on supplies originally exempt from VAT. Sometimes, acting in good faith alone is not enough to justify a company’s tax position. Too much trust in its business partners and ignorance of the law can sometimes result in liquidation penalties.

In practice, during a tax audit, we often encounter a scenario where the views of the tax administrator (tax authority, tax inspector) develop differently from the position of the tax subject (VAT payer, trading company, etc.) declared in the tax return and fail to reconcile them. Subsequently, such a dispute is decided by the court: the regional administrative court, the Supreme Administrative Court of the Slovak Republic, the Constitutional Court of the Slovak Republic or the Court of Justice of the European Union.

A new trend in the decision-making practice of the Slovak courts, which has been noticeable in the EU for a long time, is a departure from the tendency to primarily examine the (non-)fulfilment of the substantive conditions for the creation of a right to deduction. Instead, the focus is shifting to VAT fraud, where the State loses funds through the deliberate and targeted actions of the entities involved in the fraud. The following messages follow:

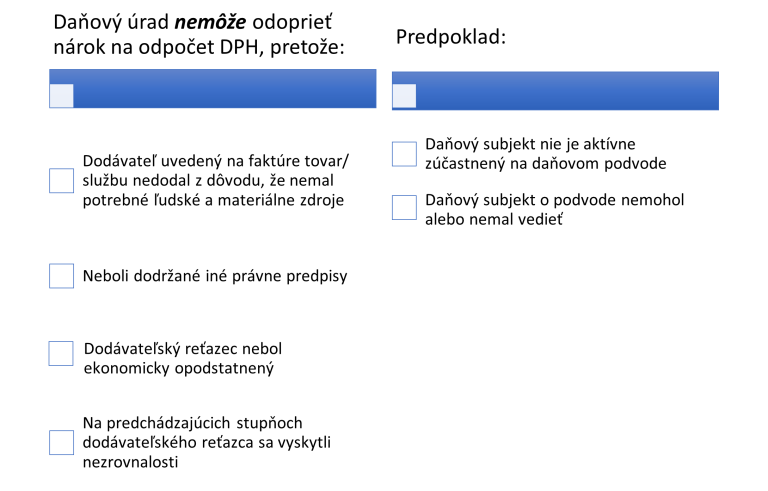

In its decision C-610/19 Vikingo, the CJEU addressed the scope of the circumstances in which a taxpayer’s right to deduct cannot be limited. Vikingo is a wholesaler of confectionery which claimed a VAT deduction on the packaging machines it purchased. However, after checking with the suppliers, the tax authorities concluded that the machines had been acquired from an unknown person, so that the supply had not been made between the persons named on the invoice.

In order to qualify for the deduction, the substantive conditions (the goods or services have actually been supplied, the recipient has used them in the course of his economic activity) and the formal conditions (primarily the existence of an invoice) must be met. In the case cited above, the Court concluded that it was not possible to deny the right to deduct VAT on the ground that the invoices were not reliable on the ground that:

However, this is assuming that the company is not involved in the tax fraud and could not and should not have known about it (see below for more on bad governance).

It follows from the above judgment that the taxable person claiming the right of deduction is not liable for the subcontractors and should not bear the consequences of any irregularities at the upstream stages of the supply chain. Nor does the tax administration have the right to refuse a VAT deduction on the basis of its (often subjective and more or less emotional) conclusion that the supply chain does not have an economic justification. A VAT deduction is also to be granted where there are doubts about the supplier’s ability to carry out the supply because of insufficient staff and material resources.

However, all of the above applies provided there is no VAT fraud in the chain.

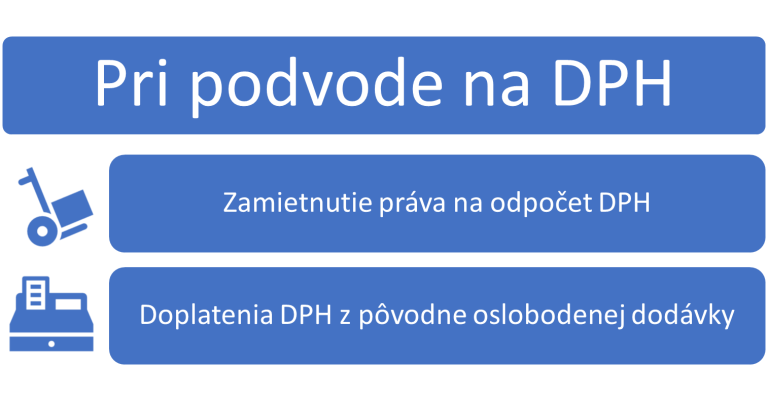

The aim of the fraud is to collect VAT from the state budget without complying with the obligation to pay it, usually at another stage of the supply chain.

So-called

Carousel frauds have different schemes of operation, but their aim is to reclaim more VAT from the State budget than to remit VAT to the State.

They use white horses, foreign companies and cross-border transactions, a combination of input VAT deduction and exempt supply at the output, fictitious transactions and invoices, significantly inflated prices and the inclusion of a genuine and honest company in the carousel.

The ambition of this blog is to raise awareness of the risks of engaging in VAT fraud transactions and to provide tips to help avoid engaging in such illegal transactions. It is important to be aware of what the consequences of engaging in a set of fraudulent transactions may be, even if these transactions are not illegal in themselves:

The CJEU has ruled in several decisions that a claim for deduction may be refused if the taxable person was part of a chain in which VAT fraud was committed, if the taxable person actively participated in the fraud (even though he or she may not have directly benefited financially from it) or knew or should have known that the transactions carried out were part of the fraud.

In Case C-439/04 Axel Kittel, the Court of Justice developed the following algorithm applicable to tax fraud:

Under the objective test, fraud is proven. This may be the case where the supplier has failed to declare the supply on his tax return or has declared it but has deliberately failed to pay his tax liability. It also combines fictitious invoices, either directly with the taxable person under examination or as input invoices with his supplier.

The subjective test examines the active or passive involvement of the taxpayer in the fraud. An indication of knowledge is e.g. an unusually low price, a personal connection, a non-standard approach to the tax entity by the supplier, a non-existent legal or natural person, payment to an account in another country, etc.

The Due Diligence test then examines how the tax entity has verified the supplier and how it has responded to any indications of risk. Of course, the written documents proving the manner and extent of the verification before or during the transaction under review are particularly relevant in a tax audit.

The concept from the Axel Kittel case law has been adopted in other decisions of the CJEU as well as in the decision-making work of administrative courts in the Slovak Republic.

The CJEU has ruled in several cases concerning VAT fraud that:

The tax authorities shall apply the principles set out in those cases where they are satisfied, having regard to objective factors, that the taxable person knew or ought to have known that he was involved in a transaction involving VAT fraud and failed to take all reasonable steps within his power to prevent his own involvement in that fraud.

A frequent finding in tax audits is that the taxpayer fails to prove the entitlement to VAT exemption. Especially critical is the situation when goods are supplied to another Member State and the supplier does not have sufficient evidence of the supply of goods with transport outside the Slovak Republic, or the customer does not acknowledge the supply in his own State.

A seemingly simple situation hides many aspects that need to be taken into account when claiming and documenting the exemption, such as. whether the transport is provided by the supplier, the customer or the postal company, whether the transport is carried out by the customer’s own means of transport, what documents are certified by the customer, how the contractual terms are agreed, how and when the customer’s VAT registration is checked.

A useful aid in setting up processes to eliminate the risks of non-recognition of exemption is the EU Regulation on the documentation of exemption, which sets out for each type of transport a set of documents that create a rebuttable presumption of proof of exemption, thus significantly narrowing the possibilities of the tax administrator to require more and more documents proving exemption.

The tax authority may require the taxable person to reimburse the tax that should have been paid by the supplier who supplied the goods or services to the taxable person, even if the invoice has been paid to the supplier. The institute of liability for tax arises in the following situations:

When defending against a possible recourse on the grounds of liability, it is important to have documents proving that the legal conditions for liability were not met at the time of delivery or payment, e.g.

the price did not show signs of unreasonableness or the supplier’s bank account was published in the relevant lists of the Financial Administration of the Slovak Republic.

Thus, it is not sufficient to carry out the verification alone, but it must also be documented and be able to be proven in the event of tax proceedings.

For a successful long-term operation, it is advisable for the tax entity to know where its potential tax risks are. This includes, for example, an analysis of how the business operates in terms of tax and specifically VAT aspects. Subsequently, the identified weaknesses need to be eliminated by appropriate procedural or commercial-legal adjustments.

For example, in order to prevent VAT fraud and tax evasion, it is beneficial for the tax entity to set up and actually carry out and archive checks on its business partners.

Business partner checks are also recommended for reasons other than tax, e.g.

In order to eliminate the risk of non-payers and reputational risk.

If you are interested in this topic, please do not hesitate to contact us.